A Difficult Transition for the Global Auto and Mobility Industry Just Got Harder and More Uncertain

Authors: By Anil Khurana and ManJune Han

The global automotive industry is undergoing one of the most significant transformations in its 140-year history. The shift from internal combustion engine (ICE) vehicles to electric and software-defined mobility solutions is reshaping supply chains, business models, and competitive dynamics. However, this transition is proving far more complex than anticipated. While some countries –most notably China – are accelerating their electric vehicle (EV) adoption through coordinated industrial strategies, others face regulatory fragmentation, slowing demand, and supply chain constraints.

In our ongoing discussions within the Baratta Center’s Global Automotive and Mobility Industry Transformation Working Group, we are examining how this transformation is shaped by a confluence of industry and macroeconomic forces, including technology advancements, global value chain restructuring, shifting consumer behavior, financial constraints, and evolving trade and policy landscapes. The question is no longer whether the transition will happen, but which companies and regions will lead—and which may struggle to keep pace – how can the industry “change all four tires while driving at top speed on a foggy highway?“

The Industry Transformation

The shift from a hydro-carbon economy with its electro-mechanical centric ICE vehicles to a zero-emission or net-zero economy wherein vehicles are powered by pure electric, hydrogen, or other fuel systems, is also accompanied by the parallel development of electronic and chemical technologies with full digital elements such as connected vehicles, autonomy, comprehensive software-based control, real-time updates of vehicles using over-the-air (OTA) updates, and so on – which are the genesis of the software-defined vehicle (SDV) paradigm.

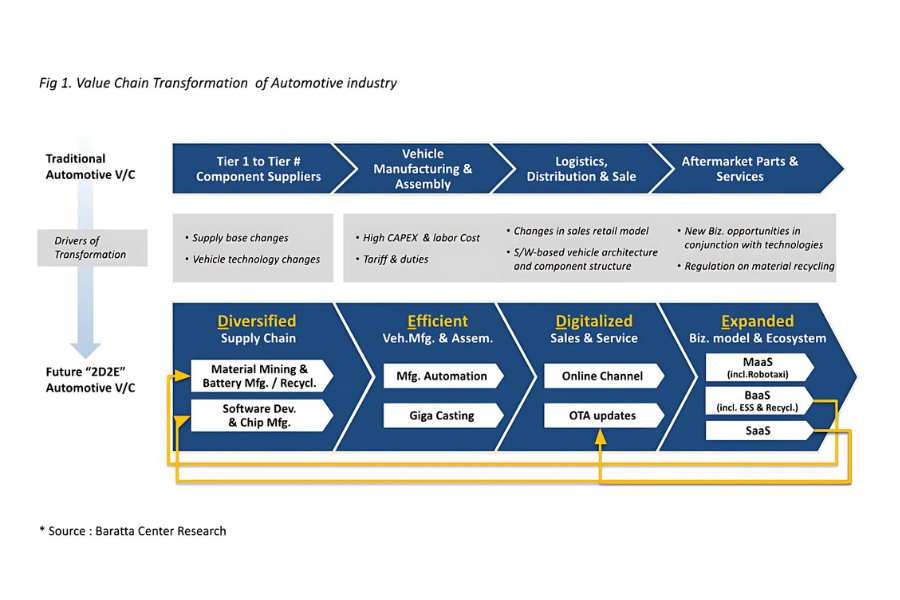

Figure 1 depicts this shift, from the traditional hierarchical value chain (of how the cars of yesterday were built) to the emerging electrified and digital value chain (with the connected and electric architecture and flatter value chain).

Figure 1. Value Chain Transformation of Automotive Industry

However, this transition requires transformational changes in the industry:

- substantial investments and changes across the entire automotive value chain – managing both the ICE vehicle architecture and supply chain, as well as the completely new EV/ ZEV value chain. Almost all facets of the global value chain require modification and expansion, and investments.

- new sets of skills and capabilities for almost every part of the new (EV and SDV) paradigm and value chain, as the bottom half of Figure 1 suggests.

- different approaches for legacy OEMs/ suppliers versus new entrants – legacy OEMs face the “innovators’ dilemma” of needing to protect their stable ICE and hybrid businesses while competing with “clean sheet” startups such as Tesla, Rivian, Lucid, BYD, NIO, Xpeng and others.

Global Risks and Challenges further complicate this Industry Transformation

In parallel with the industry transformation, the current consumer, macroeconomic, policy, trade, and geopolitical trends are key to shaping the industry’s future.

Consumer Adoption Slowdown: EV adoption rates remain uneven, with China and parts of Europe leading, while other markets face stalled growth due to range anxiety, affordability concerns, and inadequate charging infrastructure. While initial adoption by early adopters enabled a 12% EV global penetration rate for new vehicle sales in 2023, EV sales have slowed down since the end of 2023, and given the recent executive orders by President Trump, this slowdown could continue for the time being, especially in the U.S.. EV cost parity with ICE vehicles is also key, and projections of $80/kWh for LFP battery chemistries by 2030, give hope. OEMs like Toyota and Hyundai continue to hedge by adopting hybrid and plug-in hybrid (PHEV) models which have helped them maintain strong sales and profitability despite slowing EV growth.

Regulatory Uncertainty: The policy landscape varies significantly across regions, creating challenges for automakers navigating different regulatory environments. China has maintained long-term incentives and substantial infrastructure investments, providing stability for the industry. In contrast, shifting policies in the U.S. and Europe—such as adjustments to net-zero targets and reduction or elimination of incentives—have introduced uncertainty, making it difficult for companies to plan long-term investments and production strategies.

Supply Chain and Trade Disruptions: The automotive sector remains highly dependent on critical minerals, semiconductors, and battery components—and the rest of the industry’s very global supply chains—making it vulnerable to geopolitical tensions, trade restrictions, and protectionist policies (such as the recent EU tariff discussions with China, and US executive orders against Mexico and Canada). As the U.S., Europe, and China implement new industrial strategies, companies must adapt to evolving trade barriers and localization requirements.

Need for Investments: Most OEMs and many tier-1 and other suppliers find themselves in the midst of a perfect storm, which has placed unbearable financial demands on them, as many of the recent announcements on capex investments, revenue projections, and earnings by the likes of VW, Ford, GM, Nissan, and even Tesla indicate. Developing the new technologies for EV/ ZEV – e.g., batteries, motors, charging systems, software architecture, and others – place significant financial and innovation demands while EV demand has been slow to take off. At the same time, intensified competition in a shrinking pie, coupled with additional capex requirements triggered by supply chain resilience and industrial strategy (protectionism) makes the task of automakers even more difficult.

These shifts are leading to two distinct and divergent models of industry transformation: China’s state-driven, coordinated and orchestrated approach and the more fragmented, market-led path in the U.S. and Europe, with inconsistent government and policy participation.

Changing Competitive Landscape, Geopolitics, and Imperatives for Automotive OEMs and Global Supply Chains

These pressures naturally lead to different responses; some automakers have positioned themselves to capitalize on the shift toward electrification, digitalization, and new business models, while others remain focused on legacy ICE (internal combustion engine) and hybrid technologies.

China’s EV Leadership and the Challenge for Legacy Automakers

China’s automotive sector has benefited from a coordinated industrial strategy, positioning companies such as BYD, NIO, and Xpeng at the forefront of EV (and SDV) innovation. These firms have built cost-competitive, vertically integrated supply chains—reducing dependence on external suppliers and achieving rapid economies of scale.

By contrast, Western automakers must navigate a more uncertain policy environment. Companies such as Volkswagen, Ford, and Toyota are balancing investments in electric vehicle platforms with continued reliance on ICE and hybrid sales to maintain profitability. Some, like Toyota and Hyundai, have prioritized hybrid solutions as a transitional strategy, while others, including General Motors and Volkswagen, are making significant but costly EV investments.

Readiness for a Geopolitical and Policy-Driven Decade

Auto industry executives will need to enhance their approaches to navigate the complexities of public policy and an increasingly interconnected and politically charged global landscape, ensuring its long-term viability and competitiveness.

To prepare for a decade where geopolitics will dominate trade and related issues, automakers must stay agile by monitoring geopolitical developments and aligning their strategies with emerging trade policies and international relations. Auto industry executives need to adopt a multifaceted approach that emphasizes resilience, adaptability, and collaboration. Manufacturers are already beginning to diversify their supply chains to mitigate risks associated with geopolitical tensions and avoid over-reliance on any single region such as China or suppliers such as CATL, particularly for critical components like semiconductors and batteries.

Collaboration with governments on national security initiatives, such as securing domestic sources of rare earth metals, will be crucial. Further, fostering partnerships with governments and other industries can facilitate access to resources and infrastructure. And, with trade barriers and export controls likely to increase, investing in localized production capabilities can also strengthen government relationships and reduce transportation costs.

The industry will also need to proactively engage in policy discussions and advocate for incentives, favorable trade agreements, and infrastructure investments. Long-term coordination between the public and private sectors will also be essential to ensure a regulatory environment that supports sustainable growth and technological advancement.

Financial Pressures, The Need for New Skills, and Industry Partnerships

Financial Capacity and Resilience are equally important for both legacy OEMs and new entrants: For both, it is about balancing profitability and innovation, but in different ways, to ensure the ability to respond to future market shifts. For legacy OEMs, a balanced approach is one of managing their ICE, hybrid, and battery-electric portfolios, by continuing to focus on traditional ICE and hybrid sales and profitability, while investing in R&D and supply chains for battery-electric vehicles and SDVs. For new entrants, the priority is to conserve cash and accelerate the path to profitability, while continuing to innovate. The key for both groups is to have a clear view and internal alignment on what the future product portfolio looks like, say over the next decade, and develop scenarios for decision-making.

Need for New Skills: The new EV architectures – with batteries and electrified powertrains replacing petrol engines and mechanical transmissions – require new designs, manufacturing methods, suppliers, and cost structures. Similarly, today’s connected, intelligent, and software-defined vehicle requires a mastery of software and digital mobility ecosystems. Automakers and suppliers have not had it easy as they’ve invested in in-house software development, over-the-air update capabilities, and AI-driven autonomous technologies.

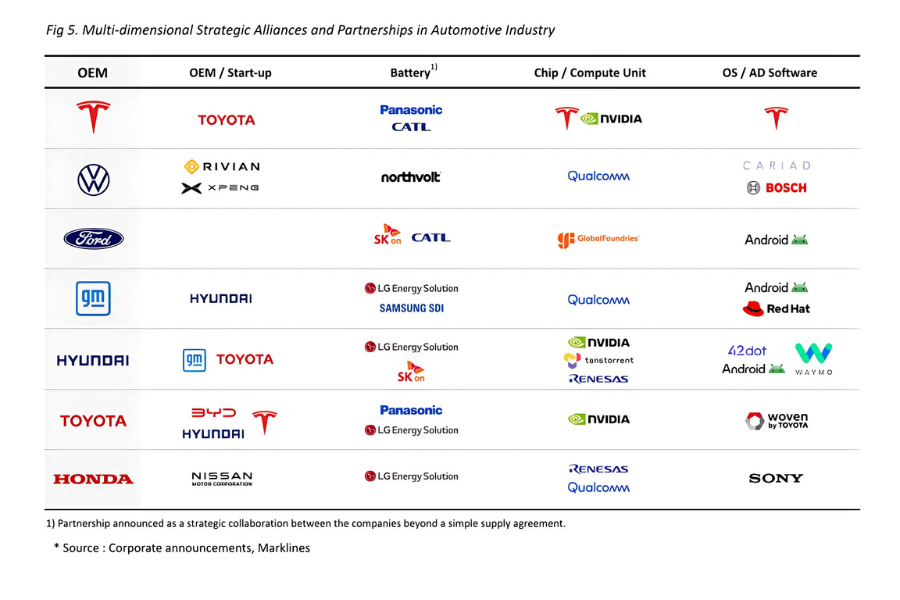

Strategic Alliances are Increasingly Necessary: Depending on the OEM’s size and balance sheet, these scenarios may involve partnerships and co-investments with legacy suppliers and other OEMs, as Honda and Nissan recently tried – and the failed alliance also points to the complexity of such relationships. A similar approach could be used to develop future EV battery systems by partnering with battery manufacturers, e.g., Volkswagen’s investment in Rivian and XPENG to co-develop E/E architectures, GM’s alliances for not only pursuing global joint ventures with battery companies such as LG and Samsung but also with Hyundai on collaboration across the entire value chain. At the same time, the software-defined vehicle (SDV) era is reshaping competition, with tech giants—including Apple, Google, and Huawei—also entering the automotive space, and triggering a range of partnerships, such as BMW and Tata Technologies, Bosch with Microsoft, and several others. Figure 2 is illustrative of a range of partnering strategies in the industry considering the significant skill set and financial requirements.

Figure 2. Multi-dimensional Strategic Alliances and Partnerships in Automotive Industry

In Summary

As the automotive industry navigates this complex transition, the future hinges on adaptability, innovation, and strategic collaboration. While China saw the opportunity more than a decade ago and was able to “orchestrate” the transition and the building of the new ecosystem, the U.S. and E.U. replied largely upon market mechanisms and have likely fallen behind.

The uncertainty during this transition also means that while companies like Tesla, BYD, and Rivian are leading the charge with their agile, software-driven approaches (and China Inc. has gone all-in here), traditional giants such as Toyota, GM, and Hyundai are balancing their ICE and hybrid models with investments in electric vehicles (EVs).

Consumer concerns, as well as stretched product and financial portfolios for OEMs and suppliers, add further pressure, and have already triggered diverse partnerships and some industry consolidation is on the horizon. Additional pressures come from unexpected twists such as diverging government policies across regions like the U.S./EU/China as well as challenges related to supply chain disruptions and geopolitical tensions, such as the U.S.-China trade wars.

Join our mailing list to be notified when new blogs come out. Sign Up for Updates.

- We use “auto/ mobility” to describe the legacy auto industry along with the evolving “zero emission” vehicles and business models which include electric vehicles (EV, BEV, hybrid), hydrogen fuel cell, etc. and innovative models and innovations like ride sharing, software-defined vehicle (SDV), and others.

- In Fig 1, under “Efficient Manufacturing & Assembly”, “Unboxed Process” indicates an auto manufacturing and assembly process that assembles vehicles from pre-made subassemblies rather than building the car on a conveyor belt. This method is more flexible and efficient than traditional assembly line methods. https://www.caresoftglobal.com/thinking/the-unboxing-methodology-for-bevs/, https://www.forbes.com/councils/forbesbusinesscouncil/2024/09/26/unboxed-assembly-a-potential-game-changer-for-auto-manufacturing/

- Tesla – Sustainable Energy for all of Earth is 10T USD – ‘Master Plan 3’ (Apr 2023); Hyundai – 120.5T KRW over the next 10 years (approx.10B USD/yr) – ‘CEO Investor Day’ (Aug 2024); Kia – 38T KRW by 2028 (approx. 6B USD/yr) – ‘CEO Investor Day’ (Apr 2024); Toyota – 12.9B USD for EV/ AI/ SCM in the financial year ending Mar 2025 – Nikkei Asia (May, 2024); VW – 180B Euro through 2028 (apprx. 40B USD/yr) – Reuters (Feb, 2024); https://www.reuters.com/business/autos-transportation/volkswagen-invest-around-180-bln-eur-through-2028-handelsblatt-2024-02-06/

- According to EV Outlook 2024 researched by BloombergNEF, “Lithium-ion battery pack price outlook”