AI and Opportunities for Local Talent in the Gulf: Disruptor or Catalyzer?

Artificial intelligence (AI) continues to shape the global economy in multiple ways. Its potential for innovation and efficiency is evident, even if tempered by adoption dynamics, yet its implications for jobs and the future of work are complex and uncertain. U.S. experts, policymakers, and political leaders recognize the potential of AI to transform multiple industries, trigger disruptive changes for the economy and labor markets, and shape national security considerations, especially against China.

For Gulf economies — particularly Saudi Arabia and the UAE — the challenge is even more critical. Saudization and Emiratization policies are beginning to make a noticeable difference in the participation of citizens in the private sector, just as AI begins to reshape the very nature of work itself. Several categories of jobs will change dramatically, and yet others may stay the same, while new jobs are expected to be created in several old and new sectors. Policy responses will need to understand the anticipated shifts in market demand for different skills, roles, and jobs, and accordingly help reshape both education and career priorities for citizens, and also the approach toward expatriate participation.

AI Adoption in the Gulf Cooperation Council: Gradual, Not Disruptive: Gradual, Not Disruptive

Despite international headlines, AI’s immediate effect on Gulf labor markets has been limited as of mid-2025. Initial implementations have focused on automating customer service, human resources, and basic analytics. As an example, the UAE government now issues work permits in seconds, and over 75% of call centers use chatbots. Yet adoption has been uneven – individual adoption is significant at about 80%, with much lower organizational adoption and impact, consistent with the recent MIT “State of AI in Business 2025” report, which highlighted the key reasons for why the return on investment is woefully low in 95% of AI business implementations. Early deployments in the Gulf Cooperation Council (GCC) have shown expected challenges: need for localization, cultural nuances, and organizational inertia have slowed widespread adoption.

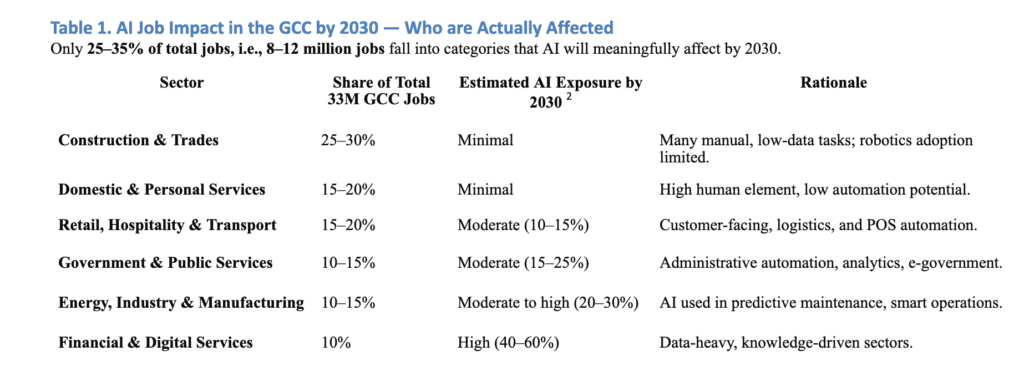

The GCC’s total workforce is about 35 million, and approximately 25-35% of these jobs — roughly 8-12 million — are expected to be meaningfully exposed to AI by 2030 (Table 1). Within this segment, AI is expected to create around 1.0–1.3 million new jobs while displacing 0.4-0.7 million existing ones. Most remaining roles — roughly 21-25 million — particularly in construction, logistics, domestic work, and other manual sectors, will see insignificant direct impact.However, in coming months and years, the roles likely to be most affected by AI-driven efficiency in the GCC are junior and mid-level white-collar positions, a large majority of these being expat roles. However, these are also the same roles that new Saudi and Emirati job market entrants are being trained for (see Table 2). Hence, GCC policymakers are already under pressure to try and maintain employment opportunities for nationals, even as they target AI-driven productivity improvement and innovation.

Beyond Digital: AI’s Potential Benefits for the Physical Economy

In 2014, Peter Thiel famously expressed his concern that innovation had advanced significantly “in bits but not enough in atoms.” The GCC’s long-standing emphasis on diversification from an oil-based economy has set the stage for a key balance in the region’s approach. The GCC’s past investments as well as future plans reflect a balance between both digitization as well as investing in the fundamental sciences – food, materials, energy, and others.

Hence, investments in AI leadership will enable not only the digital industries, but also physical-world industries — from data centers and renewable energy to manufacturing, logistics, and construction. Hundreds of thousands of new types of jobs will emerge across engineering, energy, sustainability, manufacturing, advanced materials, infrastructure, and biotechnology supply chains. It is estimated that by 2035, over 600,000 incremental jobs will be created in the GCC, with perhaps half of them being brand new types of engineering and technical roles.

Jobs and Careers for Nationals and Expats in the Age of AI

The GCC has approximately 35 million total jobs (78:22 male to female split), with ~23 million (66%) being in the private sector and 12 million (34%) in the government sector. GCC citizens represent ~85% of the government sector jobs and 16% of the private sector, and 20% of the total (or 6 million, with a 60:40 male to female split).

Nationalization in the GCC has been an important goal, but the use of quotas and targets has been a bit of a blunt instrument — guaranteeing employment without preparing the right mix of people for private-sector jobs results in inefficiencies and policy failures. AI will magnify this imbalance, especially as it reduces the demand for traditional white-collar roles and rapidly creates demand for new sets of skills and expertise. If the demand for such future skills is misunderstood, and education and training systems fail to keep pace, companies will face talent shortages that will in turn threaten nationalization goals. If expatriate hiring is restricted too quickly, private-sector AI deployment will also slow down.

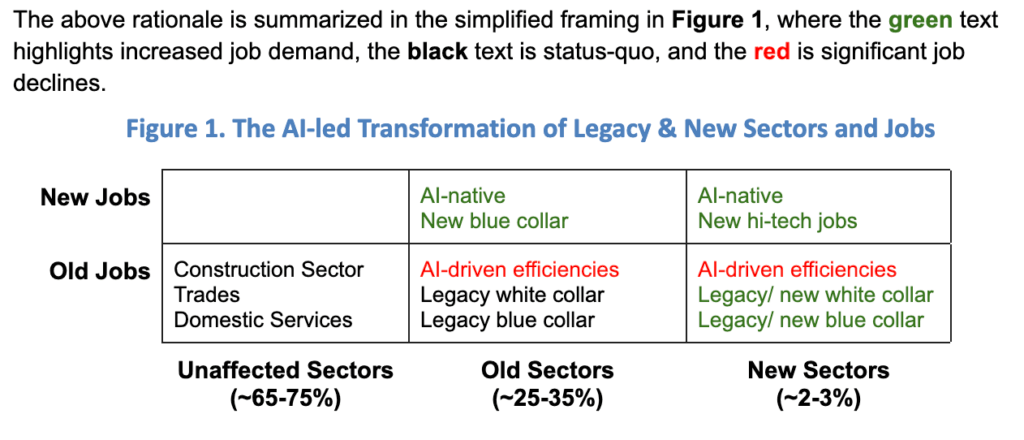

GCC regional studies suggest a four-way reconfiguration of employment. As summarized in Table 1, about 65-75% of the 35 million total jobs are expected are unlikely to be affected much by AI over the next 10 years or so. Of the remaining 25-35% jobs that will be affected by AI, roughly 20% of white-collar roles (5-7% of the total 35 million jobs), such as accountants and clerks, are declining. Another 20% — including teachers, nurses, engineers, and lawyers — require significant upskilling (so approximately 1.5-2% of the 35 million jobs). A final category comprises entirely new technical, blue-collar, and white-collar professions: AI specialists, robotics technicians, EV engineers, and data scientists. The above rationale is summarized in the simplified framing in Figure 1, where the green text highlights increased job demand, the black text is status-quo, and the red is significant job declines.

Examples of unaffected sectors include construction and personal services; “old” sectors include retail, transport, hospitality, energy, industrials, etc.; and “new” sectors include data centers, digital services, crypto, gaming, and others. Sources include the 2025 WEF Future of Jobs Report and the UAE Strategy for Artificial Intelligence.

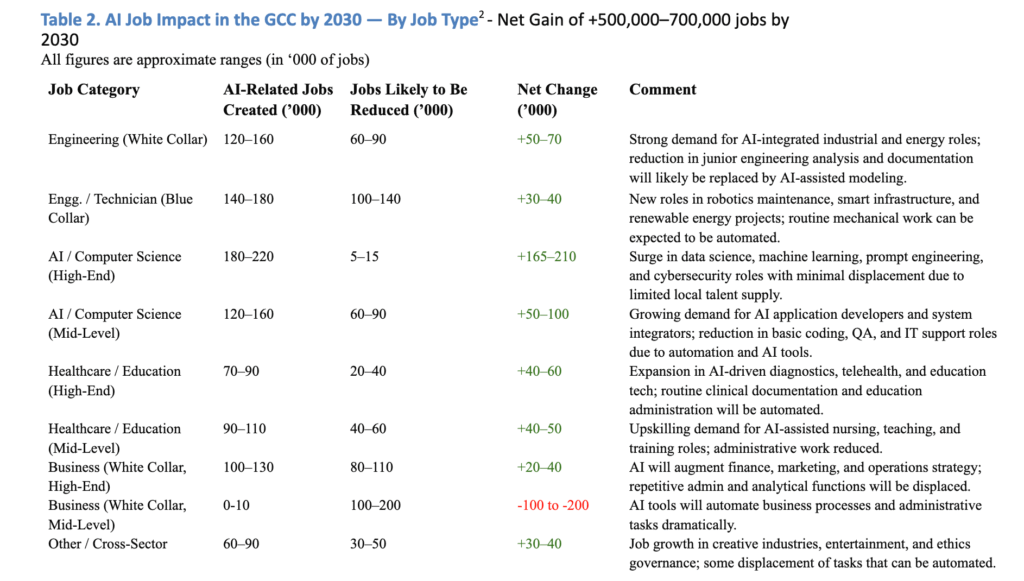

The analysis in Table 2 used this framing of job creation and job obsolescence – classic Schumpeterian creative destruction – along with changes in the types of jobs and trends and impacts in different industries and sectors. To clarify, these numbers only focus on the sectors and types of jobs directly affected, and the 20-25 million other jobs that are less affected are not included in the AI-focused analysis.

Table 2 provides a set of demand-side indications and projections that can help shape education and training policy for the GCC over the next 5-10 years. Enabling government policies will be needed soon, given that the lead time for developing and seeing the results of vocational, higher education, and on-the-job programs is typically five-to-10 years. These policies will need to ensure the availability of qualified instructors and teachers, a targeted recruiting approach amongst nationals to ensure the supply side, and employer incentives and mandates. As an example, the Saudi Data and AI Authority (SDAIA) has already trained more than 300,000 nationals, with a goal of one million by 2030. Surveys indicate that up to 60% of Saudis and Emiratis would accept lower pay in exchange for AI training — an encouraging signal of readiness to adapt. Expat and visa policies can use these inputs, along with other considerations such as real estate and entrepreneurship, to modify visa and immigration targets.

Governments must also acknowledge cultural factors, including the growing participation of women, now representing over 20% of the workforce and well positioned to lead in STEM-related fields. Further, citizens must be prepared to enter high-tech and white collar, as well as technical blue-collar roles, many of which were once undervalued or inaccessible.

The Misalignment Challenge: Individual vs. Organization

Across the world — and increasingly within the GCC — there is a clear misalignment between individual and organizational AI adoption. The MIT State of AI in Business 2025 report provides some evidence for this. The pattern holds in the Gulf. Individual professionals use tools such as ChatGPT, Claude, and Gemini to speed up research, drafting, or coding. Yet these gains rarely translate into significant enterprise-level productivity.

The reasons are largely structural: fragmented workflows, endless pilot projects, managerial hesitation, and weak training. Many firms invest heavily in AI infrastructure but fail to integrate it into core business processes. Customer-service bots illustrate the problem — widely deployed yet often ineffective, since empathy and judgment still matter. Finance and human resources face similar challenges that demand process redesign, not just new software. The technology itself isn’t the constraint; organizations are. Individuals adapt quickly because the tools are intuitive, but scaling them across departments requires redesign, training, and leadership focus. The bottleneck is human, not technical — AI adoption is now the next phase of digital transformation, driven by governance and capability rather than flashy news and hype.

Success stories illustrate a consistent pattern: AI delivers results where environments are already digital, data-rich, and logic-based. In software engineering, for example, tools such as GitHub Copilot have accelerated coding speeds by more than 50%, reducing costs and cycle times. Adjacent creative disciplines like UI/UX design are less affected for now, but automation is closing in fast.

Fintech offers another example. Upstart (an AI-driven auto and home insurance U.S. company) has built AI into its core operations rather than layering it on top of legacy systems. Its loan-approval model uses thousands of data points — education, work history, income — to expand access for underbanked borrowers while cutting defaults. Yet even Upstart faces regulatory scrutiny over the “black-box” nature of AI decision-making. Transparency and explainability remain vital for public trust.

A Narrow Strategic Window

GCC policymakers recognize well that AI is not a job destroyer but a catalyst for higher-value work. About 70% of the region’s 33 million jobs will remain largely unaffected by AI in the near future, but AI will redefine the 8-12 million jobs in the white collar and technical segments. Many of these will be higher end jobs — creating around 600,000 better-paid, more productive roles, that certainly help with the GCC’s economic diversification agenda. Saudi Arabia’s Vision 2030 and the UAE’s AI Strategy 2031 offer a brief window of time to realign education, training, and management with this shift. The real test is whether Saudization and Emiratization can evolve from quota systems to capability-building, turning disruption into long-term competitiveness rather than resistance.

Table 1 Sources

1 World Bank & ILO (2024). World Development Indicators and ILOSTAT Employment by Sector Database. Aggregated labor force and employment data for GCC economies, 2023–2024 editions. https://ilostat.ilo.org/, https://databank.worldbank.org/id/25b2e99e

World Bank Portal (2024, other). https://data.worldbank.org/indicator/SL.IND.EMPL.ZS; https://genderdata.worldbank.org/en/indicator/sl-empl-zs?utm_source=chatgpt.com&year=2023&employmentSector=Services&gender=total

Gulf Labour Markets, Migration, and Population (GLMM) Programme (2023). Total Employed Population by Sector of Employment (Public, Private, Domestic) in GCC Countries, 2010–2023. Gulf Research Center, Geneva.

GLMM — GCC labour market dashboards https://gulfmigration.grc.net/

Strategy& (PwC Middle East) (2023). Private Sector Participation in the GCC: The Workforce Challenge. PwC Middle East Ideation Center Report.

National Statistical Agencies (2023–2025). Labour Force and Employment Bulletins — General Authority for Statistics (Saudi Arabia), Federal Competitiveness and Statistics Centre (UAE), Planning and Statistics Authority (Qatar), National Centre for Statistics and Information (Oman), Civil Service Bureau (Bahrain), and Central Statistical Bureau (Kuwait).

2 Largely based on the author’s interviews with GCC industry executives and experts. Most GCC studies have focused on automation, with an initial set of studies on AI, such as UAE’s Workforce 2025: Korn Ferry Survey (https://www.kornferry.com/ae/insights/uae-workforce-report-2025)

Jobs Created ≈ 880,000–1,130,000 | Jobs Reduced ≈ 400,000–600,000 | Net Gain ≈ +700,000 jobs by 2030 (across jobs; 8-12 million affected).

Table 2 Sources

1 Author analysis and illustrative estimates, based on GCC labor market data, regional policy reports, and international benchmarks. There are millions of existing jobs – government and non-government – that won’t be affected significantly across all these job categories.

Arabian Gulf Business Insight: https://www.agbi.com/analysis/ai/2025/09/middle-east-companies-letting-down-staff-on-ai-readiness/

World Economic Forum: Future of Jobs Report 2025 – https://reports.weforum.org/docs/WEF_Future_of_Jobs_Report_2025.pdf

By Anil Khurana

Executive Director of the Baratta Center for Global Business Education;

Research Professor of the Practice