Rewiring the Road Ahead: How Mexico Continues to Shape North America’s Automotive Future

Jerry Haar1

Baratta Center Visiting Faculty Fellow

Eric Porras1a

Professor, EGADE Business School, Mexico

Few regions — and few industries — have been more profoundly shaped by globalization than North America’s automotive sector. For the United States, Canada, and Mexico, the auto industry remains a cornerstone of economic vitality: driving job creation, manufacturing output, and regional trade.

Today, as trade policy takes center stage in North American economic strategy, the industry faces a complex set of challenges across the value chain — from sourcing and production to operations and sales to the transition to zero-emission vehicles. Amid this shifting landscape, Mexico is emerging as a key player in redefining the future of automotive manufacturing and competitiveness across the continent.

Mexico’s Automotive Sector at a Glance

For Mexico’s auto industry, four key factors are likely to shape the North American competitive landscape in the immediate future: nearshoring opportunities, electrification2, the increased competition from China, and the prospect of renewal of the United States–Mexico–Canada Agreement (USMCA).To begin with, it’s important to grasp the size and scope of the Mexican auto industry. Mexico is the seventh-largest vehicle manufacturer globally and the largest in Latin America, accounting for approximately 4.7% of Mexico’s $1.8 trillion GDP in 2024 and 21.7% of manufacturing GDP3. The industry provides direct employment to over one million people, representing 22% of all manufacturing jobs in Mexico4.

Production volumes exceed three million units, and the industry demonstrates capacity utilization exceeding 95%. The automotive landscape encompasses 21 major vehicle manufacturers and 90 of the world’s 100 largest auto parts companies5. Recent investments by Audi, BMW, and Tesla, among others, underscore the sector’s growth trajectory6.

Mexico’s automotive trade relationships are predominantly North America-focused, with 92% of vehicle exports shipped to the United States, Canada, and Germany. The sector generated $52 billion in automotive exports in 2023, representing approximately 25% of Mexico’s total manufacturing exports. Foreign direct investment (FDI) flows into the country’s automotive industry over the past five years have totaled $26.1 billion, with China emerging as an increasingly important investor after the United States at $2.2 billion (18.3% of total investment), behind Germany’s 19.3% and FDI co-leaders Japan and the United States, each with 31.4%7. This reflects Mexico’s strategic position as relevant to both Asia and North America.

The Nearshoring Opportunity

The primary force reshaping the competitive landscape of North American automotive investment and production — particularly for Mexico — aside from electrification and zero emissions, is nearshoring. For Mexico, this trend, which was amplified after COVID and further in 2025 due to the global tariffs imposed by the United States, offers automakers and suppliers several strategic advantages: proximity to the U.S. market, competitive labor costs, a broad network of free trade agreements, and well-established industrial clusters. As a result, many firms that might have otherwise manufactured in Asia or other regions are now investing in Mexican operations to better serve the North American market.

Between 2022 and 2024, a wave of announcements underscored the nearshoring trend — from auto parts suppliers building new plants in Mexico to high-profile decisions like Tesla’s plan to locate its next Gigafactory in Nuevo León, or Volkswagen and Audi’s billion-dollar expansion of the Puebla plant. Other auto companies from Japan, South Korea, and Germany, in particular – pending the European Union-Mexico zero-tariffs trade agreement ratification – have shown growing interest in establishing operations in Mexico to serve both the USMCA region and global markets. Transportation alone is a compelling advantage: shipments from Mexico reach U.S. destinations in just two to five days, compared to more than six weeks from Asia.

One clear indicator of opportunity is the surge in foreign investment tied to nearshoring. In the auto parts sector, nearshoring accounted for a 15.1% increase in FDI in the first half of 2024, and the year closed with FDI in auto parts up 20% over the prior year. Automotive executives overwhelmingly report active projects to localize production in Mexico: in a late-2024 industry conference poll, 78% of automotive logistics experts said their companies were investing in nearshoring in Mexico, with nearly a third describing the investment as “significant”8. This reflects a broad consensus that relocating supply lines to Mexico is a current reality, not just a future plan.

Many suppliers setting up in Mexico aim not only to serve U.S. assembly plants but also to support the growing Mexican domestic market and even export from Mexico to South America or Europe. In the last few years, domestic vehicle sales in Mexico have picked up again, and imported vehicles (especially from Asia) have increased competition. This has prompted automakers to consider producing more models locally to better compete based on cost and avoid import tariffs on fully built units. Nearshoring thus feeds a virtuous cycle: a more robust local supplier base makes it more attractive for original equipment manufacturers (OEM) to manufacture additional models in Mexico, which in turn creates more opportunities for parts makers. As indicated in industry surveys, most automotive firms expect their Mexico-based operations to grow in the coming years — and in no small part due to technology as a contributing factor. According to Rakesh Shalia, an expert in global automotive supply chains and vice president of marketing and communications at FedEx, technology has significantly improved supply chain efficiency by providing real-time tracking, enhanced security, and proactive problem resolution, allowing businesses to optimize their operations.9

How is Mexico Positioned in the EV Market?

In Mexico, this segment of the automotive sector is clearly growing, with passenger vehicle adoption moving faster than commercial EVs. While EV sales are but a small part of the market at present (8%), EVs are poised for increased growth, having jumped more than 80% in 2024 to about 140,000. On the commercial side, things are more tentative. A few logistics fleets are experimenting with electric vehicles; in fact, some electric buses are running trial routes in Mexico City, Guadalajara, and Monterrey. Admittedly, the usual challenges exist — EVs cost more up front, insurance costs continue to be higher than internal combustion engine (ICE) vehicles, chargers outside big cities are scarce, and changes in policies make investors cautious[1]. The truth is that if Mexico wants to hit the 2030 target of 50% electrified sales, it will need greater support, such as consistent subsidies, power grid upgrades, state-support for investing in a rapid infrastructure rollout, and otherwise supporting the EV ecosystem.

Not content with merely importing EVs, Mexico also wants to build EVs locally. In just a few years, production jumped from just a few thousand units to more than 200,000 units in 2024. As for 2025, Mexico could close out the year with production of 250,000 vehicles[2]. Leading car companies such as BMW are committed to EV production. Their investment in a battery-pack plant in San Luis Potosí is a testament to that fact. At the same time, the government is trying to back homegrown bets like the “Olinia” project. Additionally, hundreds of Tier 1 and 2 suppliers are producing a range of components — everything from brake systems to control units.

Mexico has a slew of assets that provide it with a significant advantage in EV production: lithium in the ground, cheap labor, and USMCA trade rules tilted in its favor. Still, there are issues — in fact, impediments — that cannot be overlooked. Tesla’s gigafactory is delayed, policies are often unclear and change too often, and scaling local content to meet export rules is likely to prove harder than anticipated.

The China Factor — Both Competitor and Investor

A second force shaping the North American automotive landscape is the China factor. Mexico has increasingly emerged as a competitive and advantageous manufacturing hub, surpassing China in several key areas. These advantages — especially prominent in the automobile and auto parts sectors — are driven by proximity to the U.S. market, favorable trade agreements, cost competitiveness, and enhanced supply chain resilience.

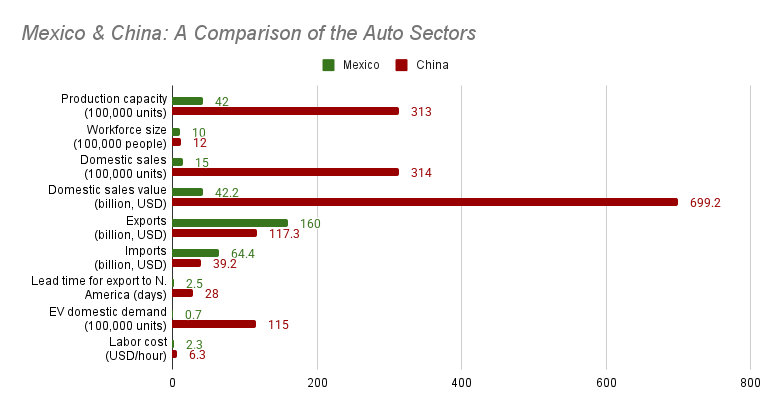

Figure 1: A Comparison of the Automotive Sector Between Mexico and China10

As Figure 1 suggests, Mexico holds several structural advantages over China in automotive manufacturing. Proximity to the United States — the world’s second-largest auto market — cuts shipping times to 2-5 days versus several weeks from China, reducing logistics costs and enabling just-in-time production. The USMCA trade agreement strengthens Mexico’s position with tariff-free access and strict rules of origin, spurring major investments such as GM’s $1 billion Ramos Arizpe expansion. Labor remains both cost-competitive and highly skilled, with average wages around $4.82/hour compared to $6.50-7.50/hour in China, supporting large-scale operations like Magna’s 32 plants. Mexico’s integrated supply chain with the United States and Canada amplifies nearshoring momentum, while BMW’s San Luis Potosí facility and Tesla’s Gigafactory in Nuevo León showcase how manufacturers are leveraging Mexico’s supplier base and renewable energy to lower costs, simplify logistics, and align with industry sustainability goals.However, the competitive threat from China should not be underestimated. Chinese companies have become significant investors in Mexico’s automotive sector. As of May 2025, Chinese investment in Mexico’s auto parts and electrical components sector surged 77% over the past year, reaching $3.9 billion. China is also a competitor in EV manufacturing and battery production, mobility, and software11.

Over the past decade, China has reshaped Mexico’s automotive market, overtaking the United States as its largest car exporter and capturing 20% of new car sales by 2024 — up from virtually zero in 2017. Chinese-made vehicles, often priced at half the cost of U.S.-built models, are now sold through GM’s joint ventures and fast-growing brands like BYD, which plans 100 dealerships by 2025. This surge threatens both Mexican production and established brands, while raising U.S. concerns about transshipment under the USMCA. In response, Mexico imposed a 50% tariff on Chinese imports in September 2025 to prevent China from using Mexico as a backdoor to North America. Although no Chinese automaker yet manufactures cars in Mexico, their suppliers are heavily invested, and the Chinese government has mounted a strong challenge to the Mexico and U.S. tariffs creating potential dependencies and geopolitical risks as negotiations for local production accelerate.

USMCA Renewal — Rules, Risks, and Realignment

The USMCA, enacted in 2020 as NAFTA’s successor, is the backbone of Mexico’s auto industry. Its rules of origin and labor standards reshaped production strategies, most notably the requirement that 75% of vehicle content be sourced from North America to qualify for tariff-free trade. That provision has spurred billions in investment but also created disputes — most prominently when the United States adopted a stricter interpretation of how to count core parts, a position rejected by a 2022 dispute panel in favor of Mexico and Canada’s more flexible approach.

The agreement faces a critical joint review in 2026, effectively a renewal decision point for extending it to 2036. For Mexico, the stakes are high: tariff-free access to the U.S. market underpins the sector, yet shifting U.S. trade policy has already injected volatility. Some companies have paused investments pending clarity, with Mexico’s bankers warning that “uncertainty kills investment.” Labor rules add further complexity: the $16/hour wage requirement for 40-45% of vehicle content has narrowed Mexico’s cost advantage and increased compliance burdens, potentially deterring labor-intensive production.

Looking ahead, the renewal debate is likely to focus on strengthening North America’s competitiveness against China. Proposals include new EV-specific rules of origin and stronger incentives for nearshoring. At the same time, Washington has signaled growing concern about Chinese automakers using Mexico as a backdoor into the U.S. market, ensuring that Chinese investment in Mexico’s auto sector will be a flashpoint in renewal negotiations.

Conclusion

In essence, Mexico’s strategic location, trade agreements, competitive labor, and robust automotive supply chain make it a superior destination for manufacturing compared to China, especially for automobiles and auto parts. Companies such as BMW, Ford, General Motors, and Tesla exemplify how manufacturers leverage Mexico’s advantages to enhance competitiveness, meet regulatory requirements, and optimize operations.

Despite the tension and uncertainties surrounding the global political economy, the North American automotive industry is poised for growth and transformation, driven by EV adoption, technological innovation, and supply chain realignment. Even though EV adoption in the United States is currently experiencing a slowdown — due to vehicle prices, inadequate charging infrastructure, and policy uncertainty surrounding government incentives and regulations — the trend is irreversible. As automotive manufacturer Bocar’s CEO Marcus Baur notes, “Mobility and connectivity will continue to shape the future of the automotive industry, with digital platforms playing an increasingly central role in business models.”12

Collaborative efforts between companies and governments in the United States, Mexico, and Canada will be critical to maintaining global competitiveness and sustainability in this rapidly evolving sector. To reshape North America’s automotive sector, emphasizing Mexico’s critically important role in this process, individual and collective action by government, the private sector, business associations, and educational institutions must work arduously to alleviate barriers and improve performance in the automotive sector across a number of domains — mainly, technology (especially EVs and batteries), geopolitics, trade, and supply chains.

References

1Jerry Haar is a professor of international business and faculty advisor for executive education in the College of Business, Florida International University. He’s also a senior fellow for the Council on Competitiveness.

1a Eric Porras is a professor of operations, logistics and supply chain at EGADE/Tec de Monterrey

2Electrification along with the emergence of the software defined vehicle are expected to increase in importance in coming years.

3Manufacturing is approximately 20% of Mexico’s GDP: https://tradingeconomics.com/mexico/gdp-from-services.

4https://napsintl.com/manufacturing-in-mexico/industries-in-mexico/#:~:text=Major%20Manufacturing%20Industries%20in%20Mexico,textile%2C%20and%20consumer%20products%20industries.

5Key global brands including Audi, BMW, Ford, General Motors, Honda, Kia, Mazda, Nissan, Stellantis, Toyota, and Volkswagen maintain significant production operations across 14 Mexican states.

6Tesla’s planned Gigafactory in Nuevo León represents a $5-10 billion investment targeting production of one million vehicles annually. BMW committed $855 million to its Nuevo León facility for electric vehicle production beginning in 2027, while Audi announced $1 billion in EV investments at its Puebla plant.

7https://www.americanindustriesgroup.com/news/mexico-sets-record-foreign-direct-investment-in-2024/; https://mexiconewsdaily.com/news/fdi-mexico-2024/; https://www.statista.com/statistics/948616/foreign-direct-investment-automotive-industry-mexico/.

8https://www.automotivelogistics.media/event-highlights/alsc-mexico-2024-investment-in-nearshoring-continues-in-mexicos-automotive-supply-chain/185118#.

9Interview with Rakesh Shalia, March 17, 2025.

10All figures, except the labor cost, pertain to 2024. Data taken from multiple sources, including OICA 2024 Country Report for ‘All Vehicles’ for current production capacity, Marklines International Platform and Gasgoo News Report for domestic sales, Data Mexico Platform and Reuters Report (which includes all vehicles including chassis) for exports, China-CEEC Customs Information Center for imports, Mexicom Logistics and Dimerco Platform for export lead times (projected as the simple mean of the reported intervals), Mexico Business News Report and CNEVPost Report for EV domestic demands, Prodensa Report, and some other news reports, such as IBISWorld, and QUARTZ, for workforce size and labor costs.

Value figures in USD are not readily available for domestic sales. For the purpose of this comparison, they are calculated as follows: for Mexico, the total number of units times the average unit price of each. For China, we have the sales value from the National Bureau of Statistics of China. Finally, they’re expressed in 2024 USD terms following the exchange rates from the Federal Reserve.

11https://mexicobusiness.news/automotive/news/mexico-auto-parts-sector-sees-77-rise-chinese-investment

12Interview with Marcus Baur, February 10, 2025