The Growth Dilemma: Standing Between Venture and Buyout in Private Equity

By Kishor Moorthy (B’25)

In 2023, over $100 billion was invested in growth equity, making it one of the fastest-growing categories within private equity1. Despite its larger presence, growth equity has received limited attention in academic research compared to venture capital and buyout private equity. As a senior at Georgetown University’s McDonough School of Business entering the private equity world, I sought to explore whether growth equity truly performs differently than other strategies, which is a question with significant implications for institutional investors.

This research project, which enabled my undergraduate senior honors thesis completed in May 2025, analyzed and compared the return profiles of venture capital, growth equity, and buyout private equity funds using a data-driven approach. Here, I summarize the key findings of my study, reflect on the research experience, and highlight the invaluable support I received from Georgetown’s Baratta Center for Global Business, RockCreek, and Professor Sandeep Dahiya, a professor of finance at the McDonough School of Business.

Why Growth Equity Deserves Closer Attention

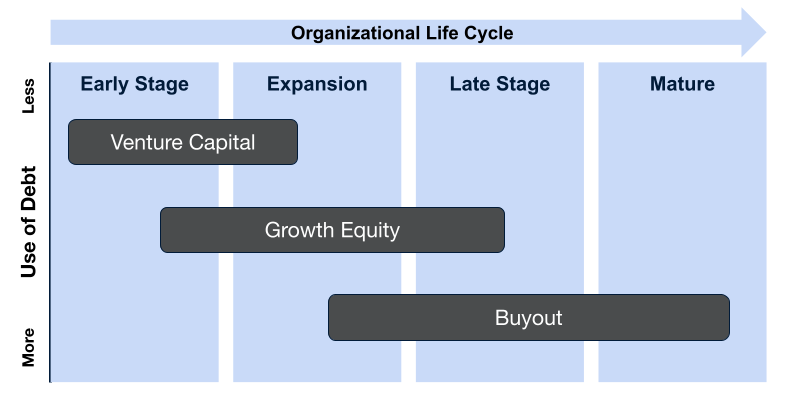

The private equity landscape is more diverse than ever, and institutional investors face increasing complexity when allocating capital across fund types. Venture capital offers high risk and potentially high reward by investing in early-stage startups. Buyout funds focus on acquiring mature businesses with leverage, offering lower yet more consistent returns. Growth equity, however, occupies a unique middle ground, targeting high-growth proven companies while avoiding the high debt levels typical of buyouts.

Figure 1: Private Equity Strategies by Organizational Life Cycle

Source: Graphic reproduced from Phalippou, L. (2020). Private Equity Laid Bare. 3rd ed. CreateSpace Independent Publishing Platform.

Despite its strategic significance, growth equity has often been lumped together with other categories in performance studies. My research set out to treat growth equity as a distinct strategy and test whether it offers superior, inferior, or similar returns compared to venture and buyout funds. The study also explores various other factors that significantly affect fund performance.

Approaching the Analysis with High-Quality Data

This study would not have been possible without the support of the Baratta Center for Global Business and its partnership with RockCreek. Through this collaboration, I was granted access to RockCreek’s Objective Data Collective (ODC), which includes proprietary private equity fund data.

“We’re always exploring new ways to analyze and learn from the 20+ years of industry data we’ve collected,” noted Matthew McMaster, managing director at RockCreek. “Partnering with Georgetown University’s Baratta Center on research projects like this one helps surface fresh insights and strengthen our understanding of evolving markets. It has been a pleasure collaborating with Georgetown faculty and students to uncover compelling trends in the private equity space.”

Data from RockCreek was merged with Bloomberg’s private equity fund database accessible through the Bloomberg Terminals on Georgetown’s campus. This combined dataset of 936 U.S.-based venture, growth, and buyout funds (vintage years 1979 to 2012) allowed for a rich comparative analysis of Net Internal Rate of Return (Net IRR) and Multiple on Invested Capital (MOIC) across strategies. Using statistical tests and regression modeling, I aimed to isolate the effect of strategy by accounting for fund size, fund sequence, and vintage year.

Key Insights from Research

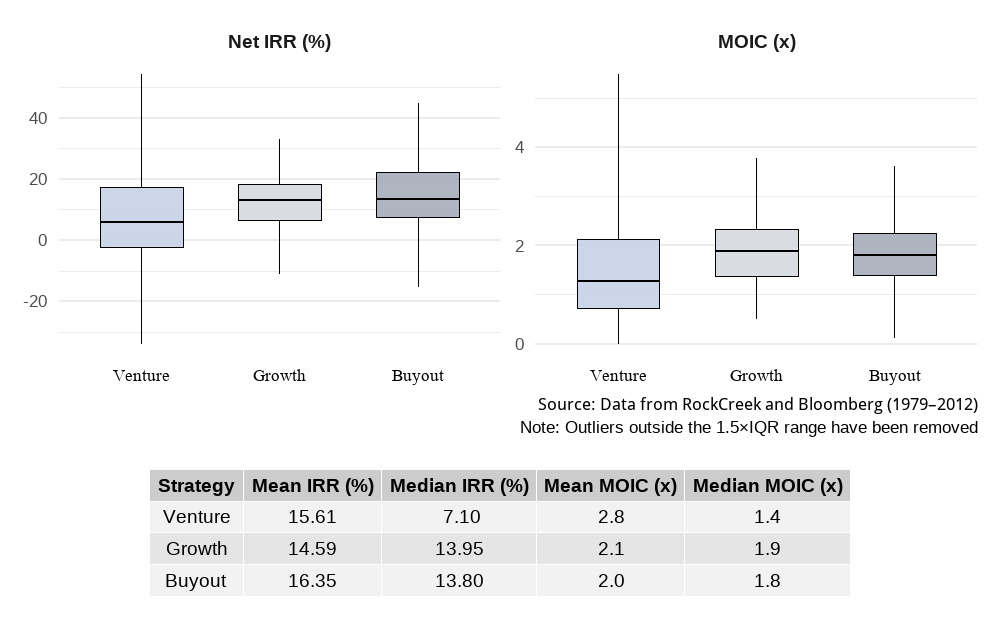

As shown in Figure 2, the summary statistics reveal that growth equity performed the best on median Net IRR and MOIC, while buyout and venture performed best on mean Net IRR and MOIC, respectively. As expected, Figure 2 also shows that venture capital returns were far more variable than buyout or growth equity funds, underscoring the higher risk profile of early-stage investing. These findings suggest that growth equity may offer a competitive risk-return profile and play an increasingly relevant role in the portfolios of limited partners (LPs) managing diversified alternative asset allocations. Growth equity has also emerged as a critical source of capital for firms looking to stay private for longer, especially as going public has become less desirable.

Figure 2: Fund Performance Descriptive Statistics by Strategy, 1979-2012

Contrary to common intuition, my regression models found no statistically significant difference in growth equity returns relative to venture and buyout funds after controlling for other factors. However, several other important patterns emerged.

One of the key areas I was interested in exploring was the relationship between fund characteristics, such as fund size and fund sequence, and performance outcomes. The analysis revealed a negative relationship between fund size and MOIC, suggesting diminishing returns to scale where larger funds may face challenges in deploying capital efficiently or maintaining discipline in deal selection. Later-sequence funds tended to perform better, indicating the value of general partner (GP) experience and investor confidence. These insights support the idea that LPs should carefully balance experience and scale when evaluating funds.

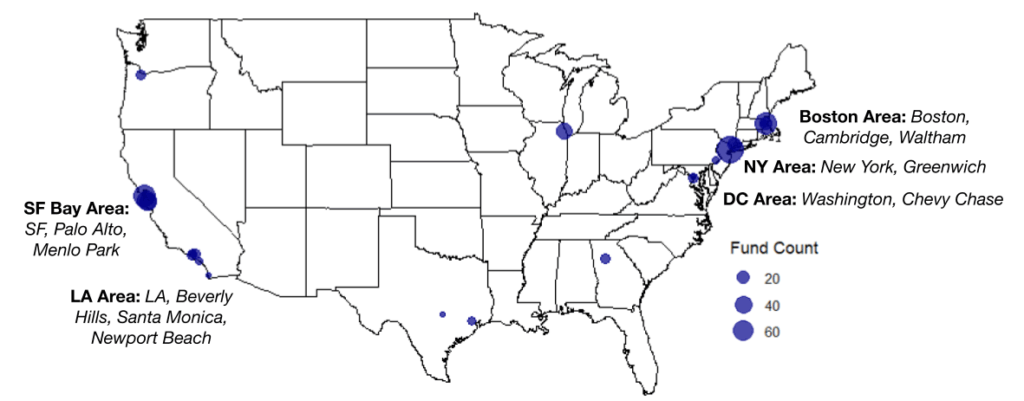

I also examined how external factors, such as fund headquarters and economic timing, influenced performance. Figure 3 shows the geographic concentration of funds based on headquarters location. Funds based in financial centers (New York, Boston, and San Francisco areas) outperformed their counterparts. Outperformance was especially strong for venture capital funds in the New York area. This performance premium is likely driven by improved access to high-quality deal flow, the ability to attract top-tier talent, and the strong network effects within these ecosystems. Furthermore, timing played a major role in performance as venture capital funds with vintage years from 1999 to 2002 underperformed significantly due to the dot-com bubble. These findings reveal that institutional investors should consider macroeconomic context and fund location when allocating to private equity funds.

Figure 3: Fund Headquarters Locations in RockCreek Sample

Source: Data from RockCreek (1979-2012)

A Unique Applied Research Opportunity at the Undergraduate Level

This project has been one of the most impactful experiences of my undergraduate career. Working with institutional-quality data and engaging in rigorous analysis gave me a realistic understanding of how research can influence investment decision-making. More importantly, it provided a unique opportunity to bridge the gap between academics and industry. The support from RockCreek and the Baratta Center enabled me to apply classroom learning and personal interests to real-world data. Finally, I cherished the opportunity to work one-on-one with Professor Sandeep Dahiya, who served as my research advisor and offered guidance driven by his industry expertise.

“It was great to undertake this journey of discovery with Kishor,” said Dahiya. “He did a great job of refining his initial hypotheses into sharply testable implications and obtaining the data to conduct those tests. The support of the Baratta Center and RockCreek was absolutely critical in this. We learned some interesting lessons – I was quite surprised that venture, growth, and buyout funds, on average, delivered similar investment returns.”

As I prepare to begin my full-time role in growth equity next year, this experience has sharpened my analytical thinking, expanded my knowledge of investing strategy distinctions, and deepened my appreciation for the complexity of institutional capital allocation.

Empowering Better Allocation Decisions

Growth equity has emerged as a critical component of modern private equity investing. My research confirms that while returns may not be significantly superior, growth equity offers a compelling middle ground that merits further exploration and attention. Furthermore, the lack of significantly different returns across strategies reveals that factors such as risk appetite, manager selection, and timing should drive LPs’ allocation to private equity funds.

- Lattanzio, G., Litov, L. P., Megginson, W. L., & Munteanu, A. (2023). Capitalizing entrepreneurship: The rise of growth equity. Journal of Applied Corporate Finance, 35(2), 75–89. https://doi.org/10.1111/jacf.12561